Data-Driven Governance: How AI Is Quietly Rewriting the Rules of Proxy Season

Updated: Apr 30

Something significant happened in January 2026 that most people outside of Wall Street barely noticed.

JPMorgan Asset Management — one of the largest asset managers on the planet, with voting rights over thousands of publicly listed companies — quietly cut ties with its proxy advisory firms. No more ISS. No more Glass Lewis. Instead, it launched an internal AI tool called Proxy IQ, designed to analyse data from over 3,000 annual company meetings and generate voting recommendations on its own terms.

Wells Fargo followed weeks later with its own internal proxy voting platform, powered by Broadridge Financial Solutions.

Two of the biggest names in institutional finance decided, within weeks of each other, that they no longer needed the firms that have shaped corporate governance for decades. That is not a routine technology upgrade. That is a signal.

So what is actually happening? And why should anyone outside a boardroom or a hedge fund care?

First — What Even Is a Proxy Season?

If you are new to this world, a quick grounding.

Every year, public companies hold annual general meetings where shareholders vote on things like who sits on the board, how much executives get paid, and whether the company should adopt certain policies. Most individual shareholders do not show up in person — they vote by "proxy," which is essentially a written instruction submitted in advance.

Because institutional investors — think pension funds, asset managers, index funds — hold enormous blocks of shares across thousands of companies, they cannot possibly research every vote themselves. That is why proxy advisory firms like ISS (Institutional Shareholder Services) and Glass Lewis grew into such powerful players. These firms analysed companies, published voting recommendations, and effectively told institutional investors how to vote. For years, a favourable recommendation from ISS was practically a guarantee of shareholder support on major votes.

That era is ending.

Proxy Season AI — Why Is AI Entering Proxy Voting Now?

The timing is not accidental. Several things collided at once.

Regulatory pressure has been building. A December 2025 Executive Order in the US directed the SEC to scrutinise proxy advisory firms for conflicts of interest, lack of transparency, and potential political bias. That gave institutional investors political cover — and arguably a nudge — to build their own independent processes.

At the same time, AI tools have matured enough to actually do this work. Analysing 3,000 company filings, governance disclosures, pay structures, board compositions, and shareholder proposals used to require an army of analysts. Today it is a workload that well-designed AI systems can handle faster, more consistently, and at a fraction of the cost.

And then there is a deeper frustration that has been simmering for years. The "one-size-fits-all" benchmark recommendation — the same vote guidance applied to every fund regardless of its specific mandate — never made much sense. A passive index fund tracking the S&P 500 has very different governance priorities from an activist growth fund or a sustainability-focused impact vehicle. AI makes it possible to actually reflect those differences in voting decisions.

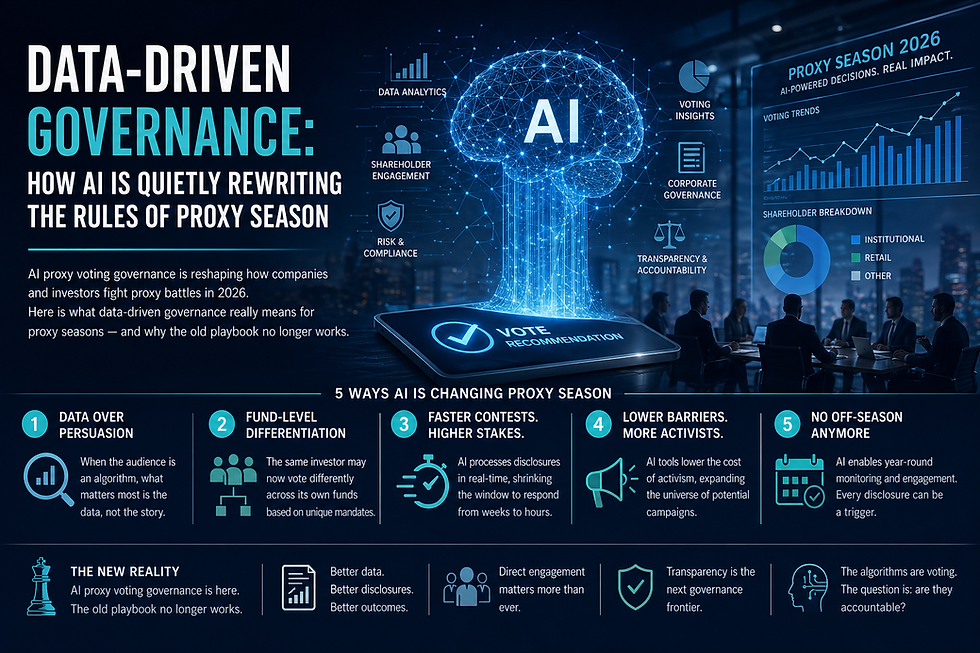

Five Ways This Changes Everything

Researchers at Paul, Weiss, Rifkind, Wharton & Garrison published an analysis on the Harvard Law School Forum on Corporate Governance in March 2026 laying out five structural shifts that AI is likely to trigger in proxy seasons going forward. Having read it carefully, I want to walk through each one — but in plain language, because these shifts matter well beyond the legal community.

1. Data will matter more than persuasion

For decades, the proxy contest was largely a persuasion game. Companies and activists crafted elaborate "fight decks" — polished presentations arguing their case — and sent them to proxy advisors and institutional investors hoping to win hearts and minds.

That game changes when the audience is an algorithm, not a human analyst.

If institutional investors are increasingly using AI to form their views, then the question shifts from "what story are you telling?" to "what data are you feeding the machine?" The inputs — which metrics the AI is trained to prioritise, which data sources it draws from, how it weights governance versus financial performance — start to determine outcomes before a single conversation happens. For companies preparing for proxy season, that is a fundamentally different challenge from writing a compelling letter.

2. The same investor may now vote differently across its own funds

This one is subtle but important. Historically, large institutional investors applied one voting policy across all their funds. You knew how Vanguard would vote. You knew how BlackRock would vote. That predictability was useful for everyone — companies knew what to expect, activists knew which investors to target.

AI enables something different: granular, fund-level voting policies. A passive index fund within the same firm might vote differently from an active strategy fund. An ESG-focused vehicle might diverge from a plain vanilla equity fund managed by the same institution.

BlackRock and State Street have already split their stewardship functions into separate teams with different mandates. The days of the predictable "house vote" — where you could confidently model how a major investor would cast its ballot across all positions — are numbered.

3. Proxy contests will move faster and hit harder

AI does not sleep, does not take lunch breaks, and does not need three days to digest a quarterly earnings release.

As companies and activists deploy AI tools capable of processing new disclosures in near real-time, the cadence of proxy contests accelerates dramatically. A company files an update on a Tuesday morning. By Tuesday afternoon, AI systems at multiple institutional investors have already flagged the implications, updated their analysis, and potentially shifted preliminary vote positions. The window for "correcting the record" before investor sentiment firms up shrinks from weeks to hours.

This places an enormous premium on being proactive rather than reactive. Companies that wait until they are under attack to craft their governance narrative are going to find the battlefield has already moved on.

4. The barriers to activist investing are falling

Running an activist campaign used to be expensive. You needed a team of analysts to screen for target companies, build investment theses, model out scenarios, draft proposals, and manage investor outreach. That kept activism largely in the hands of well-resourced hedge funds.

AI-enabled screening tools can now do a significant portion of that groundwork at a fraction of the cost and time. Which means the universe of potential activists is expanding. Smaller funds, occasional participants, and even first-time activists can now pursue campaigns that simply would not have been economically viable a few years ago.

The US saw activist campaign volumes rise approximately 19% above the multi-year average in 2025, according to Barclays research. That number is unlikely to shrink in 2026. When barriers to entry fall, participation goes up. Companies that previously felt insulated from activism because they were "too small to be worth it" may find that calculation no longer holds.

5. Shareholder engagement has no off-season anymore

There used to be a rhythm to corporate governance. Proxy season ran roughly from January through June. Companies and investors engaged intensively during that window, then largely stepped back for the rest of the year.

AI is dissolving that boundary.

Institutional investors are now deploying AI tools to continuously monitor public disclosures — earnings releases, quarterly reports, board changes, regulatory filings — and identify engagement priorities throughout the year. A surprise CEO departure in September, an unusual acquisition announcement in November, a governance red flag buried in a 10-K — these are now potential triggers for immediate investor outreach, not items to be filed away until the next proxy season.

For boards and management teams, that means year-round governance visibility. The preparation for an annual meeting now starts, in a sense, the moment the last one ends.

What Does This Mean for Companies?

The practical implications are significant and worth being direct about.

Securing a favourable recommendation from ISS or Glass Lewis no longer guarantees a smooth vote. With major institutional investors building their own AI-powered processes and splitting their stewardship teams into multiple functions, companies now need to engage with several decision-makers within a single asset manager — often with different mandates, different information appetites, and different voting priorities.

The quality of your disclosures matters more than ever. AI systems parse filings. Vague language, inconsistent narrative, or gaps between what a board says and what the numbers show will be picked up more reliably and more quickly than any human analyst would catch them. Plain, precise, and consistent disclosure is no longer just good practice — it is a defence mechanism.

And smaller shareholders are now a genuine strategic consideration. With institutional vote blocs becoming more fragmented and retail voting programmes growing in sophistication, the margins in contested situations may increasingly be determined by votes that would previously have been treated as irrelevant background noise.

What Does This Mean for Activist Investors?

The environment cuts both ways for activists.

On one hand, AI lowers the cost of finding targets, building a case, and executing a campaign. The practical barriers that once limited activism to the best-resourced funds are shrinking. That creates opportunity for new entrants and expands the range of companies that could find themselves in an activist's crosshairs.

On the other hand, the elimination of predictable "benchmark" proxy advisor recommendations makes it harder to guarantee a coalition of institutional support. Activists can no longer assume that getting a favourable ISS recommendation translates into a winning vote. Direct outreach to individual funds, fund-specific messaging, and early coalition-building now matter more than a single influential recommendation.

The quality and originality of the investment thesis also becomes more important in a more competitive landscape. When more actors can run activist-style analyses, the ones who succeed will be those with genuinely differentiated insights — not those who can simply marshal the most capital or the loudest campaign.

The Question Nobody Is Really Asking Yet

Here is something that deserves more attention than it is currently getting.

As voting decisions migrate from human analysts at proxy advisory firms to AI systems built inside institutional investors, the transparency of the governance process actually decreases. With ISS and Glass Lewis, their methodologies — even if imperfect — were published. Companies and activists could study them, understand what drove recommendations, and engage accordingly.

With proprietary AI systems built inside individual asset managers, that transparency disappears. Nobody outside JPMorgan's stewardship team knows exactly how Proxy IQ weights its inputs, which data sources it draws from, or what assumptions are baked into its recommendations. The same will be true for every institution that builds its own system.

This is not a reason to stop the shift — the old system had serious problems of its own, including conflicts of interest that regulators have documented at length. But it does create a genuine governance challenge: how does the market hold AI-driven voting accountable? What recourse does a company have if it believes an AI system is systematically mis-weighting its governance quality? How do shareholders themselves know whether their votes are being cast in their best interests?

These are not rhetorical questions. They are the next frontier of the governance debate, and the regulatory frameworks to address them are still essentially blank pages.

Where Does This Leave Us?

Corporate governance has always been a lagging indicator of broader shifts in finance and technology. The structures that shaped proxy seasons for the past two decades — proxy advisory duopolies, standardised benchmark recommendations, predictable institutional vote blocs, clearly delineated proxy seasons — grew up in a world of information scarcity and high analytical costs.

That world no longer exists.

What is replacing it is faster, more fragmented, more personalised, and in some ways more unpredictable. Companies that adapt early — by improving disclosure quality, building direct investor relationships year-round, and understanding how their governance narrative translates into data signals — will be better positioned than those still playing by the old rules.

Activists who invest in genuine analytical edge, rather than relying on proxy advisor leverage, will find more opportunity and face more competition simultaneously.

And the rest of us — shareholders, employees, pensioners with money in index funds — have every reason to pay attention to how AI is being used to govern the companies whose shares sit inside our portfolios. Because the algorithms making those calls are increasingly doing so without asking us.

Win the New Proxy Season with AI-Ready Governance

Is your organisation prepared for a world where AI shapes shareholder voting?

Join the upcoming webinar by Directors’ Institute – World Council of Directors and learn how to strengthen disclosures, engage investors, and stay ahead in a data-driven governance era.

👉 Secure your spot: https://www.directors-institute.com/webinar-registration

Comments